Can a Cyprus property settlement be financed?

Yes, if handled sensibly

Last week I put out a 10-minute video on the costs of division for both sides of the island. For your friends who are not on Substack, you can also find it on YouTube here.

One of the greatest concerns that people have about a united Cyprus is the cost of a property settlement. A property settlement needs to address the fact that, by 1974 around 30% of Greek Cypriots had been displaced to the southern part of the island and around 40% Turkish Cypriots had been displaced to the northern part of the island, leaving property on both sides. This is a huge topic in its own right and I wrote about the background here.

Preparing for the video took me back to one of the sections of the most recent of the “peace dividend” reports that I co-authored, namely Delivering the Peace Dividend, published by the Cyprus Centre of the Peace Research Institute Oslo (PRIO) in early 2020, and authored by Mustafa Besim, Michalis Florentiades and me. You can find the report here and all of the videos and infographics that went with it, in English, Greek and Turkish, if you scroll to the end of the “About us” section here.

Below I am reproducing Section 6.5 of that report called “Can a property settlement be financed?” In the section immediately before that, we had done a number of calculations based on different scenarios. These scenarios included the amount of property to be compensated (as opposed to reinstated, exchanged etc); the values awarded by the European Court of Human Rights (ECHR) versus the amount requested by claimants; the amounts awarded by the Immovable Property Commission (IPC); and estimates made by the University of Cyprus. All of this drew on a great deal of number-crunching I did while working either as a staffer or as a consultant for the UN Good Offices Mission in Cyprus.

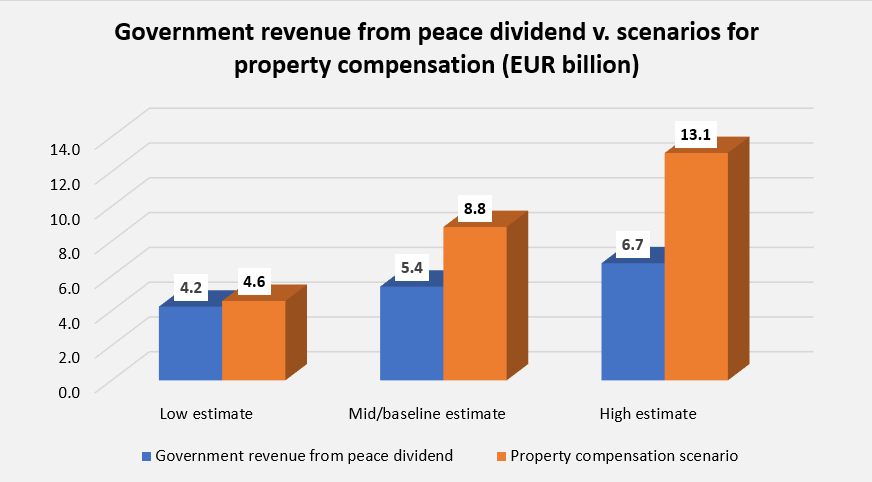

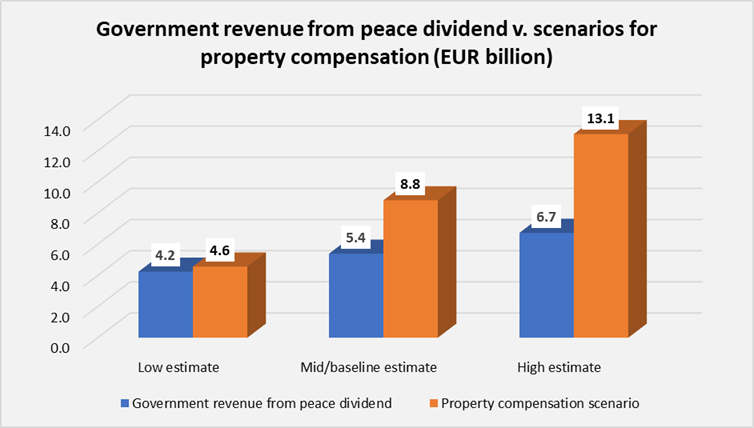

Based on these scenarios, we estimated that the property bill could range from €4.6bn to €13.1bn depending on which methodology you used for calculating compensation and how much property was compensated. We noted unconfirmed reports that the World Bank had estimated the property compensation cost, net of exchange, at €8bn. If you want to get “inside baseball”, so to speak, go to Chapter 6.4 of the full report.

Below I am reproducing in full the section that followed that, Chapter 6.5, on whether compensation could be financed. The short answer is yes, as long as the negotiators are sensible about it.

6.5 Can the property settlement be financed?

Extract from Delivering the Cyprus Peace Dividend, Mullen, Besim and Florentiades, PRIO Cyprus Centre, 2020

“Can a united Cyprus afford property compensation if it has to be financed from domestic sources? The short answer is yes, if handled sensibly. For the purposes of this analysis we assume that there will be no aid from the international community for compensation, given that Cyprus counts as a high-income country, and that any funds from Turkey for supporting a settlement may well be directed to rehousing families who might be displaced as a result of reinstatement and territorial adjustment. We therefore assume in this analysis that compensation will initially come from either the constituent state or federal government budgets. Options for raising funds over the medium term from other sources are discussed below.

As outlined in Chapter 4, our scenarios for post-settlement real GDP growth, based on two different methodologies, yield a cumulative peace dividend that ranges from around €11.0bn to €17.4 billion at constant prices. If we assume that government revenue remains fairly stable at around 38% of GDP, the government revenue “dividend” – that is, additional tax and other revenue as a result of a solution – should be between €4.2bn and €6.7bn at constant prices. In our baseline scenario, 61% of property compensation could be funded simply by the increase in the tax-take and other revenues that would come with a growing economy. In the worst-case scenario, if growth is low and negotiators go for the highest compensation scenario, then government revenue will cover only 32% of the compensation bill. In the best-case scenario (high growth, low compensation), additional revenues could cover the entire bill.

Taking the lowest compensation scenario of €4.6bn, it is worth noting that the Republic of Cyprus government spent €3.5bn in a single year in 2018 on liquidating the Cyprus Cooperative Bank according to IMF data. Moreover this cost was met without recourse to international assistance. This fact, plus the above-mentioned revenue dividend, suggests that €4.6bn should be affordable, especially if it is spread over a number of years.

Figure 6.6

Source: Authors’ estimates.

If the negotiators go to the other extreme and choose a methodology that leads to the highest compensation cost of €13bn (approximately half of all-island GDP today), then they will need to adopt several methods to avoid taking money from essential services such as health and education. They will also need to avoid economic distortions by pouring large amounts of money into a small economy in a short period. Incentives that will help reduce the federal or constituent states’ compensation bill include the following.

An online, fast-track system. In exchange for a faster payout, owners can choose to take a discount on the assessed compensation value.

Longer payment period. Stretching payments over a 30-year period via long-term bonds issued to owners. These bonds to owners could be financed on international markets. The Republic of Cyprus issued its first ever 30-year international bond in May 2019, paying a coupon (interest rate) of 2.75%.

Ownership stakes. Offers of ownership stakes in special areas designated for development instead of monetary compensation. This may be especially attractive to owners who want to exchange large tracts of land.

Contributions from current users. Revenue from current users who gain full clean title to their properties, and who thereby see the value of those properties rise, could be raised via taxation, or via a kind of mortgage that becomes payable to the government when the property is sold.

Ultimately the amount to be compensated and who pays for it will be a political decision, balancing considerations of acceptability, equity (including the impact on other stakeholders of decisions) and affordability. As long as negotiators do not take decisions without calculating the financial consequences, property compensation should be affordable.”

That was what we wrote in 2020. No doubt numbers for the peace dividend, the additional tax-take from that dividend, and the potential property compensation would be different today. But I hope it gives you an idea of the relative ratios, as well as ideas on how to keep decisions about compensation methodology out of the hands of those who do not understand economic consequences.

People sometimes approach me to ask if I am going to do an update. I confess that the idea tends to bring me out in hives. For each of the five different peace dividends I co-authored between 2008 and 2020, I under-estimated the massive amount of work involved and therefore under-budgeted for it, which meant that each new report came at great personal cost: physical, psychological and financial. Therefore, I am afraid my well has run dry: if you need ideas please go and read the old ones! You can find them all in the Publications section if you scroll to the end here.

If you want my premium monthly in-depth product, check out Sapienta Country Analysis Cyprus and other deep-dive reports here or single copies here. And if you can’t afford those but want the executive summary only for just €100/year*, you can find that here on Substack, at Cyprus Pocket Brief.

Or support this publication, Sapienta Cyprus Snippets, for just €49 per year.*

*Monthly payments are a massive administrative headache, so since I can’t switch them off I have effectively banned them by setting the monthly price the same as the annual.